Individual health insurance in Dubai is no longer optional.

1. How Much Does Individual Health Insurance Cost in Dubai (2026)?

Premiums depend on five factors: age, medical history, annual limit, network size and optional riders. For a healthy 35-year-old:

For most UAE residents, individual health insurance costs range from AED 700 to AED 8,500 per year, depending on age, benefits, and network.

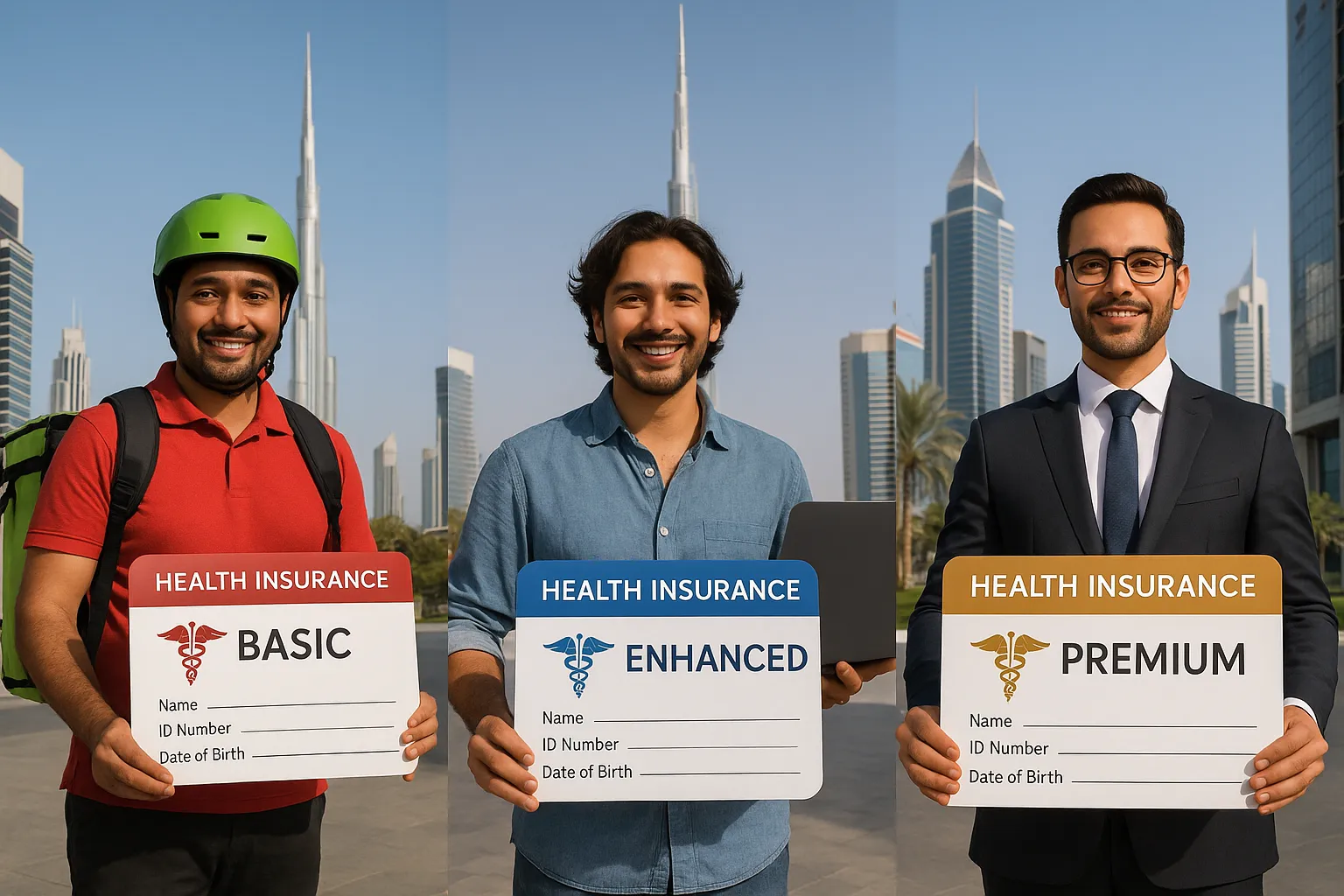

- Basic EBP: AED 700 – 800

- Enhanced: AED 1 900 – 2 800

- Premium worldwide: AED 5 000 – 8 500

Tip: pay the full premium upfront to save up to 10 %; most insurers waive instalment fees during Ramadan flash sales.

Cost per month (approximate):

Basic: AED 60–70

Enhanced: AED 160–230

Premium: AED 420–700

Get Compared Individual Health Insurance Plans in Dubai (DHA Approved)

2. What does individual major medical health insurance cover?

“Major medical” is industry slang for in-patient benefits: surgeries, ICU, chemotherapy, organ transplant, and advanced imaging (MRI/CT/PET). Dubai policies must also include:

- Emergency ambulance across the UAE

- Maternity (normal & C-section) with newborn cover

- Out-patient GP & specialist consultations

- Prescription drugs (co-pay capped at AED 1 500/year on basic plans)

Always read the sub-limits. A plan advertising “AED 1 million coverage” may restrict maternity to AED 10 000 and dental to AED 1 500.

3. How do I compare individual health insurance providers quickly?

- Visit insurancehub.ae and click Compare Plans.

- Enter basic data: Emirates ID, age, visa type, pre-existing conditions.

- Instantly view side-by-side quotes from 50 + DHA-approved insurers.

- Filter by network hospital, co-insurance, tele-medicine, or worldwide elective cover.

- Receive a call from a licensed advisor to explain fine print and issue the policy—often in under 30 minutes.

4. Can I get cheap individual health insurance with pre-existing conditions?

Yes, but expect a loading of 10–25 % depending on severity. Since 2024, DHA rules prohibit outright rejection for chronic illnesses; instead, insurers adjust premiums or impose short waiting periods. Strategies to soften the hike:

- Submit recent medical reports—clear documentation reduces perceived risk.

- Opt for a restricted network; you can upgrade after one claim-free year.

- Accept higher co-insurance (e.g., 20 % outpatient) in exchange for lower base premium.

5. Is maternity cover included automatically?

Only under DHA’s mandatory minimums. Basic plans offer ~AED 7 000 normal delivery, while premium plans cover up to AED 25 000 plus NICU. If family planning is on the horizon, upgrade before conception; a standard 6-month waiting period applies.

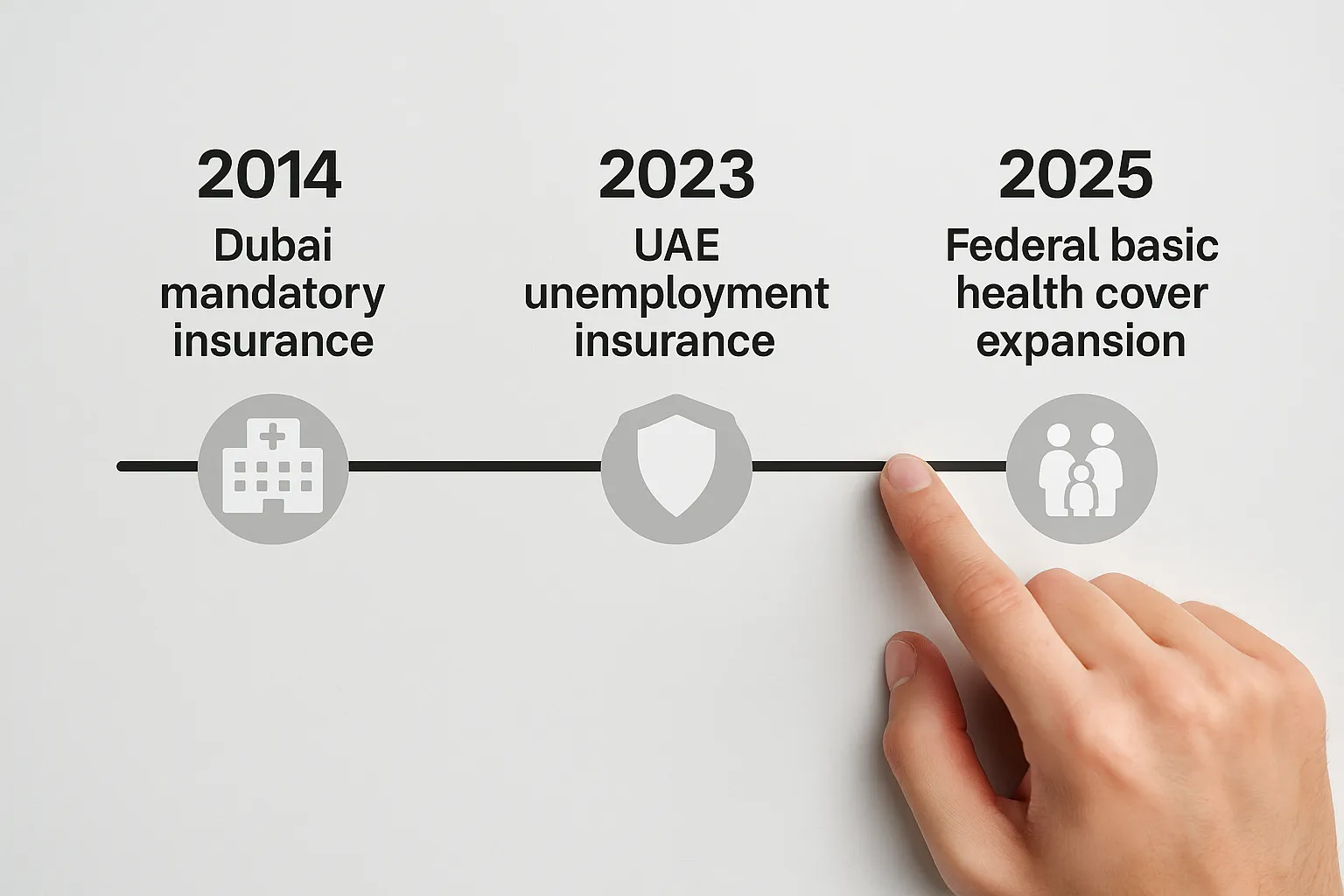

6. How do new federal rules affect individual buyers in 2025–26?

The nationwide mandate harmonises benefits across all seven Emirates, so Abu Dhabi and Sharjah residents can now buy a Dubai-structured EBP for as low as AED 320. Good news: pre-existing chronic conditions receive day-one coverage on basic plans, a first in the region.

Smart Ways to Lower Your Premium Without Sacrificing Coverage

- Annual pay vs monthly pay – save 5–10 %.

- Restricted UAE network – if you rarely travel, skip worldwide cover.

- Higher outpatient co-pay – raise from 10 % to 20 % and pocket ~15 % premium cut.

- Maintain BMI & non-smoker status – insurers offer up to AED 500 wellness cashback.

- Bundle policies – buy life or home insurance together on Insurancehub and qualify for multi-product discounts.

Claim Process in Dubai: Cashless vs Reimbursement

- Cashless: Present your e-card at an in-network hospital, sign the consent form, and the insurer settles directly.

- Reimbursement: For out-of-network treatment, pay first, then claim online within 30 days. Attach invoices, medical reports, and Emirates ID.

Insurancehub’s digital claims desk has a 97 % acceptance rate within 10 working days, versus 15–20 for industry average.

Ready to protect your health and your wallet? Compare, customise and buy individual health insurance in Dubai in just three steps at Insurancehub.ae — and join 200 000 + UAE residents who saved up to 40 % last year.