Family health insurance cost

The cost of family health insurance in the UAE is influenced by a web of variables – from each family member’s age to the size of the hospital network you choose. With mandatory nationwide coverage now in force (effective 1 January 2025), understanding exactly what drives a premium up or down is the surest way to protect your loved ones without over-paying.

1. What actually determines your family premium?

Below are the primary inputs UAE insurers feed into their pricing models when generating a family quote:

| Cost Driver | Why it Matters | Typical Impact on Premium |

|---|---|---|

| Emirate of residence | Network agreements and regulator rules differ slightly between Dubai Health Authority (DHA) and Department of Health – Abu Dhabi (DOH). | Dubai premiums are often 5-10 % higher for equivalent benefits because of stricter network standards. |

| Plan category | Basic (Essential Benefits Plan), Enhanced, or Premium. | Up to 4× cost difference between entry level and premium. |

| Age of each insured | Utilisation risk rises with age. | In most 2025 rate cards, every 10-year age band can add 12-18 % to individual cost. |

| Family size | More lives mean higher aggregate risk. | Insurers usually offer a per-member discount once you add the third dependent. |

| Pre-existing conditions | Chronic illnesses trigger higher expected claims. | Loadings can range from 10 % to 50 % or exclusion riders. |

| Coverage territory | UAE only, GCC only, worldwide excl. USA, or worldwide incl. USA. | Up to 60 % jump for worldwide coverage that includes the USA. |

| Add-ons(maternity, dental, optical) | Extra benefit limits expand claim potential. | Each add-on can add AED 800-2,000 per year to the family bill. |

| Payment mode | Annual vs monthly installments. | Annual payment discounts of 3-5 % are common. |

According to the UAE Central Bank Insurance Market Report 2024, medical inflation averaged 9.2 % last year – a major reason families see renewal premiums creep up even without making claims.

2. The regulatory baseline for 2025

The new federal mandate obliges every employer (and domestic-worker sponsor) to provide at least a Basic Health Plan that mirrors Dubai’s Essential Benefits Plan (EBP):

- Annual limit: AED 150,000 per member

- Emirates-wide emergency cover at 100 %

- Outpatient co-pay: 25 % capped at AED 100 per visit

- Inpatient co-insurance: 20 % capped at AED 500 per visit and AED 1,000 per year

- Medication co-insurance: 30 % capped at AED 1,500 per year

For families that must purchase their own policies (for example, self-employed professionals, dependents, or golden-visa holders), insurers price basic plans from AED 320 to AED 725 per person per year, depending on emirate and network.

While the Basic Plan meets legal requirements, many households upsize to Enhanced or Premium tiers for broader networks, shorter waiting periods, and maternity limits that reflect real birth costs (typically AED 15,000-25,000 in private hospitals).

3. Real-world cost scenarios for a family of four in 2025

The table below uses live rate cards from three Central Bank-approved insurers and InsuranceHub’s quoting engine (June 2025). It assumes two healthy parents (ages 34 and 32) and two children (ages 5 and 1).

| Plan Tier | Annual Family Premium (AED) | Territory | Key Benefits |

|---|---|---|---|

| Basic / EBP Equivalent | 2,600 – 2,900 | UAE only | AED 150k limit, limited network, maternity AED 10k, 30 % drug co-pay |

| Enhanced Mid-Range | 5,800 – 7,200 | UAE + GCC | AED 500k limit, 300+ facility network, maternity AED 20k, dental cleaning 1×/yr |

| Premium Worldwide excl. USA | 11,000 – 14,500 | Worldwide excl. USA | AED 1 million limit, open network, maternity AED 25k, dental & optical, wellness checks |

A quick sense-check

- Cost per member in a Basic family package is roughly AED 650-725. Enhanced plans jump to about AED 1,500-1,800 per member.

- Children are usually rated cheaper – some insurers quote kids at 50-70 % of adult price.

- Employer extensions can be cheaper than standalone family policies, so ask HR if top-ups are allowed.

4. Do not ignore the “silent” costs

A low sticker price can hide heavy out-of-pocket exposure:

- Co-pays and coinsurance – every GP visit at 25 % soon adds up when you have toddlers.

- Sub-limits on maternity, physiotherapy, or diagnostics that leave you paying the remainder.

- Waiting periods – most Enhanced plans still impose 6-12 months for maternity and 6 months for dental unless you pay extra.

- Network restrictions – driving from Abu Dhabi to Dubai for a paediatric specialist negates any premium saving.

DHA data show that over 40 % of family policy complaints in 2024 related to unexpected sub-limits rather than claim denials. Always read the Schedule of Benefits.

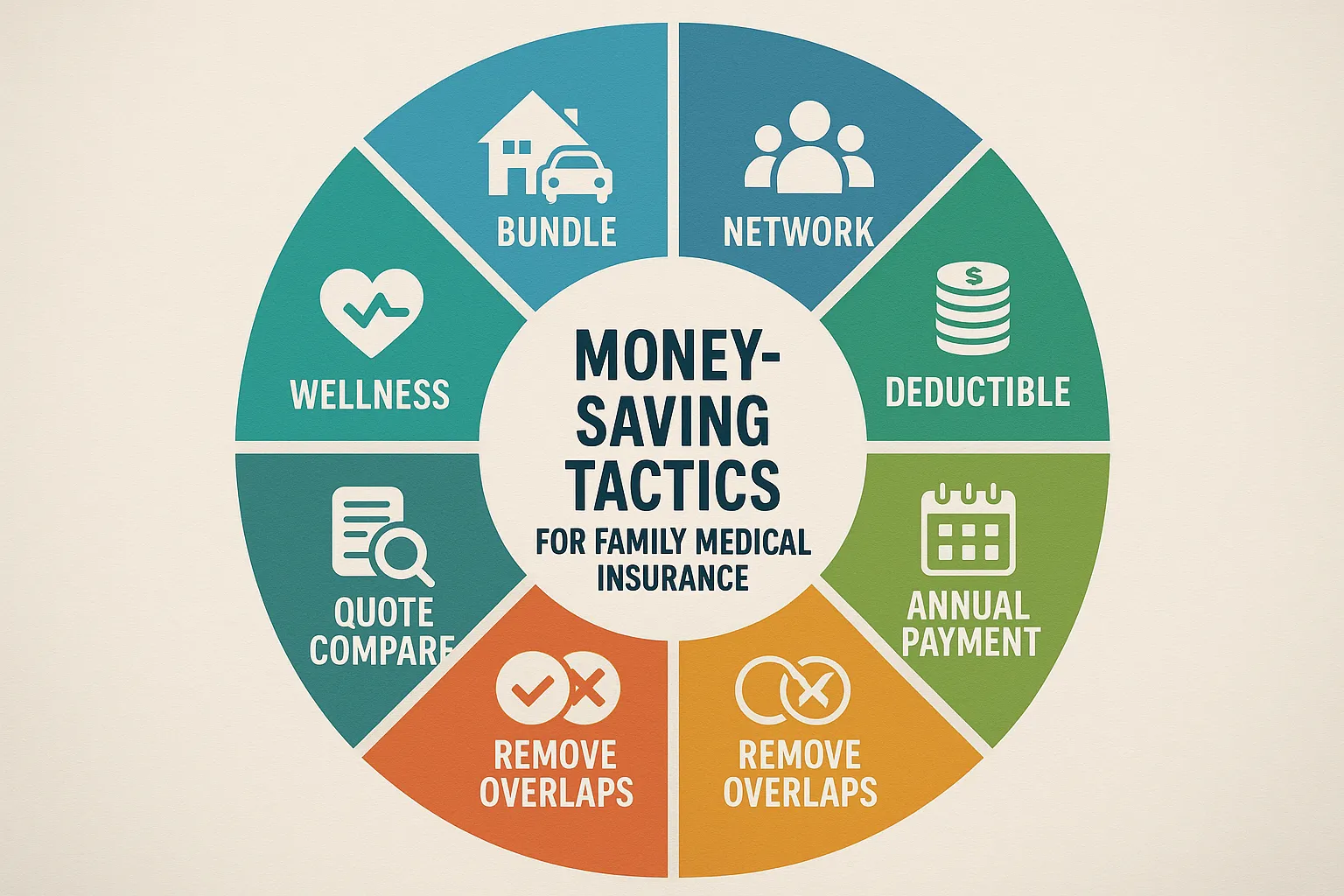

5. Seven smart ways to reduce your family’s premium in 2025

- Bundle every dependent under one insurer. Multi-life discounts can shave 5-7 % off.

- Choose restricted networks (Tier 2 or 3) for routine care but keep emergency treatment at any facility.

- Opt for higher deductibles on inpatient claims (AED 1,000+) if you have an emergency fund.

- Pay annually. Insurers reward upfront payment with lower admin cost.

- Use wellness benefits – free screenings earn no-claim bonuses at renewal.

- Compare at least three quotes online rather than accepting the first renewal notice. InsuranceHub’s engine pulls rates from 50+ insurers in minutes.

- Remove overlapping benefits if your employer already covers dental or vision for the main member.

6. When paying more is worth it

There are situations where the higher premium delivers outsized value:

- Planned pregnancy within 12 months – upgrading to a plan with no maternity waiting period can avoid AED 25-30k in private delivery costs.

- Frequent international travel – a worldwide plan may cost AED 3k extra but can save six-figure hospital bills abroad.

- Chronic disease management – broader networks mean shorter appointment queues and lower co-pays on repeat prescriptions.

If any of the above apply, treat the extra premium as preventive spending, not a cost.

7. How InsuranceHub.ae keeps family cover affordable

- Instant multi-insurer comparison – see side-by-side premiums, benefits, network size, and claim settlement ratios.

- Licensed advisors – receive personalised guidance on maternity limits, chronic condition declarations, and deductible strategy.

- Exclusive partner discounts – save up to 40 % versus walk-in retail rates.

- Central Bank-approved insurers only – peace of mind that your family’s cover meets 2025 regulations.

- Digital claims assistance – track reimbursements online to avoid paperwork delays.

For detailed plan navigation, read our guide on choosing the right family cover (Shield Your Family’s Health) or explore cost-focused tips for Abu Dhabi in the Cheapest Health Insurance 2025 Guide.

Final thoughts

Family health insurance cost in the UAE is no longer a guessing game. By understanding the variables, benchmarking real market rates, and using smart premium-reduction tactics, you can secure compliant, comprehensive protection that fits your budget. Run a free quote on InsuranceHub.ae today, talk to an expert, and lock in the right cover before the next premium cycle creeps up.