General Health Insurance in Dubai

Dubai’s skyline may scream luxury, yet even a routine GP visit can set you back AED 300–500 if you walk in uninsured. According to the Dubai Health Authority (DHA), private inpatient stays now average AED 9,000 per day (DHA Annual Report 2024). In a city where medical bills climb as quickly as the Burj Khalifa, general health insurance isn’t just a legal checkbox—it’s the safety net that keeps residents and expatriates from financial free-fall.

What Exactly Is “General” Health Insurance?

“General” (or basic) health insurance refers to the entry-level plans that meet Dubai’s mandatory coverage rules under Law No. 11 of 2013. The DHA labels this the Essential Benefits Plan (EBP). It is designed to give every visa holder access to core healthcare services—emergency, inpatient, outpatient and maternity—without piling on expensive bells and whistles.

Key characteristics:

- Annual coverage limit: AED 150,000 (raised from AED 100,000 in 2024 to reflect inflation)

- Regulated co-payments and caps on inpatient, outpatient and pharmacy bills

- Restricted but reliable provider network within the UAE

- Standard waiting periods (e.g., 6 months for maternity unless transferring from another compliant plan)

For many workers earning below AED 4,000 per month, dependents on family visas, or freelancers searching for affordable protection, the EBP does the heavy lifting at a price that won’t torpedo the monthly budget.

Dubai’s Mandatory Insurance Framework in 2025

Dubai was the first emirate to introduce compulsory medical insurance for all residents, but 2025 marks the first year every emirate has followed suit under Federal Decree-Law No. 48 of 2023. For Dubai visa holders, the rules remain straightforward:

- Employers must fund compliant cover for employees.

- Sponsors must insure dependents (spouse, children under 18, domestic helpers).

- Visa renewals are blocked if proof of active coverage isn’t uploaded to the GDRFA system.

- Fines start at AED 500 per month of non-coverage and can escalate to visa cancellation.

An upshot for consumers: competition has expanded, pushing insurers to improve service quality and digital claims tools—many now approve e-claims in under 48 hours.

For a detailed legal breakdown, see A Complete Guide to Dubai’s Mandatory Health Insurance Laws.

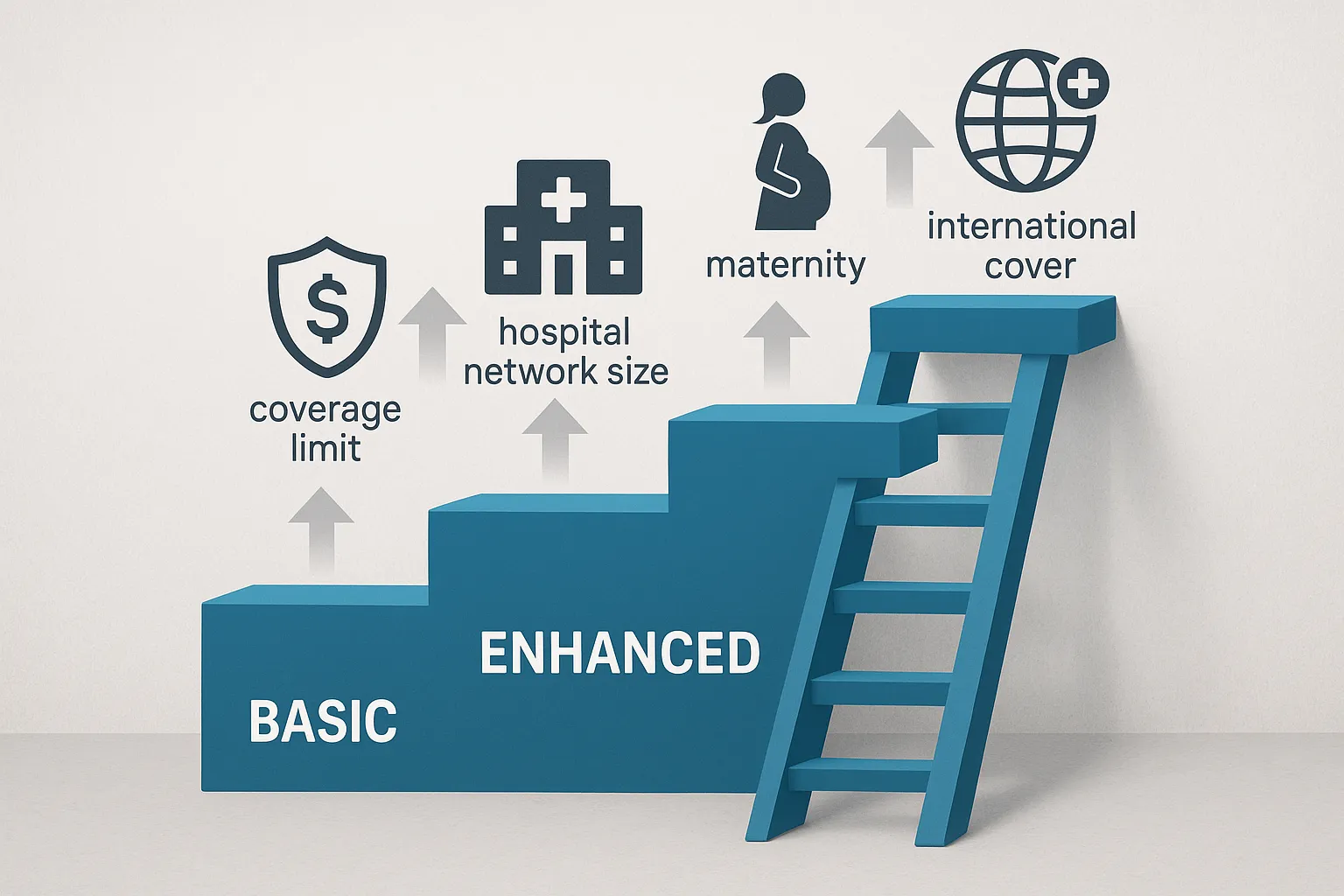

EBP vs Enhanced vs Premium—At a Glance

| Feature | Essential Benefits Plan (EBP) | Enhanced “Silver” Plan | Premium “Gold” Plan |

|---|---|---|---|

| Annual Limit | AED 150,000 | AED 250,000–500,000 | AED 1 million–unlimited |

| Provider Network | Tier III (district clinics & select hospitals) | Tier II national network | Tier I regional & worldwide |

| Outpatient Co-pay | 20 % (max AED 50/visit) | 10 % or waived | 0 % |

| Pharmacy Co-pay | 30 % (capped AED 1,500/year) | 15 % | 0–10 % |

| Maternity Cover | Up to AED 10,000 normal / AED 12,000 C-section | Up to AED 20,000 | Up to AED 40,000 |

| Overseas Emergency | Not covered | GCC only (optional) | Worldwide |

| Typical Annual Premium* | AED 725–975 | AED 1,500–3,800 | AED 5,000–12,000 |

*Premiums for a 30-year-old non-smoking resident, 2025 market survey (InsuranceHub data)

Who Should Consider General Health Insurance?

- Entry-level employees and low-income workers whose salary packages don’t stretch to employer-paid upgrades.

- Dependents—spouses, children, parents—where the sponsor wants affordable but regulated coverage.

- Freelancers and small-business owners registering their first trade licence on a tight cash-flow.

- Recent graduates and first-time job-seekers who need compliant cover to activate or renew their visas.

If you tick any of these boxes, an EBP can keep you legal and protected while you build financial stability. For supplemental outpatient scans, dental or worldwide benefits, you can layer top-ups later.

Cost Breakdown: What Will You Really Pay in 2025?

Premiums are set by insurers but capped by the DHA to remain accessible. Across 50+ licensed providers, InsuranceHub’s 2025 rate study found:

- Single adult (19–45 yrs): AED 725–975

- Child (0–18 yrs): AED 540–650

- Domestic helper: AED 650–800

Add-ons such as dental (AED 250–400) or optical (AED 200–300) are optional. Remember, co-pays apply when you actually use services—budget roughly AED 2,000 per year if you have chronic medications or frequent GP visits.

Real-World Snapshot

Case Study: Ahmad, Delivery Rider, Age 29

• Monthly Salary: AED 3,200

• Premium Paid by Employer: AED 840 (EBP)

• 2024 Claims: One outpatient clinic visit (flu) – bill AED 260 → Ahmad paid 20 % (AED 52)

• Savings vs paying cash: AED 208 in one visit; risk of larger bills eliminated

If Ahmad upgrades to a Silver plan for AED 1,950 annually using payroll deduction, he gains a bigger hospital network and lower co-pays—but would spend an extra AED 1,110 upfront. For occasional users, the basic plan makes financial sense.

Buying Smart: A 5-Step Online Playbook

- Collect your details: Emirates ID, visa copy, last insurance certificate (if any).

- Use a comparison portal such as InsuranceHub.ae to pull live quotes from 15–20 DHA-approved insurers.

- Filter by network & co-pays—not just price. Check if your preferred clinic appears on the list.

- Review exclusions: pre-existing conditions are covered from day 1 in Dubai only if the previous plan was continuous. Otherwise a 6–12 month waiting period applies.

- Purchase & receive e-card within minutes. The portal will auto-link your policy to the GDRFA visa system, so renewal goes through smoothly.

For deeper cost-saving tips, read Maximizing Your Health Insurance Benefits: Tips and Tricks for Dubai Residents.

Digital Claims & Telehealth—The 2025 Upgrade

General plans used to lag behind premium products in technology, but the gap is closing fast.

- e-Cards & e-claims: 92 % of EBP insurers now accept scanned receipts via mobile app (InsuranceHub Claims Survey Q2 2025).

- Telemedicine: Three major TPAs, including NextCare and NAS, provide 24/7 video GP consults—even on basic tiers—saving a clinic trip and the 20 % co-pay.

- AI fraud filters: Faster adjudication means reimbursement in 3–5 business days on average, down from 10–14 days in 2022 (PwC Middle East Health Insights 2025).

When Should You Upgrade?

General health insurance covers the essentials, but it may fall short if you:

- Expect a new baby and want private-room maternity cover.

- Travel frequently outside the UAE and need worldwide emergency treatment.

- Manage a chronic condition requiring high-cost biologics that could pierce the AED 150k cap.

- Prefer premium hospitals like American Hospital Dubai or Clemenceau, which sit outside EBP networks.

A rule of thumb: if projected out-of-pocket costs exceed the upgrade premium, it’s time to move up a tier. Our guide The Ultimate Guide to Finding the Best Health Insurance in the UAE for 2025 walks you through the calculus.

Final Word: Compliance Today, Flexibility Tomorrow

Dubai’s general health insurance may be “basic” by name, but it provides a solid foundation—legal compliance, first-rate emergency care, routine doctor visits—at a cost that fits most entry-level budgets. The secret is to treat it as step one in a long-term protection strategy. Review your needs annually, upgrade when life events (marriage, childbirth, chronic illness) demand more, and use digital tools to squeeze every dirham of value from your benefits.

Ready to lock in compliant coverage or explore an upgrade? Compare live quotes in minutes at InsuranceHub.ae and speak with a licensed advisor who can help you save up to 40 % without sacrificing peace of mind.